SBA Loans: Who Qualifies?

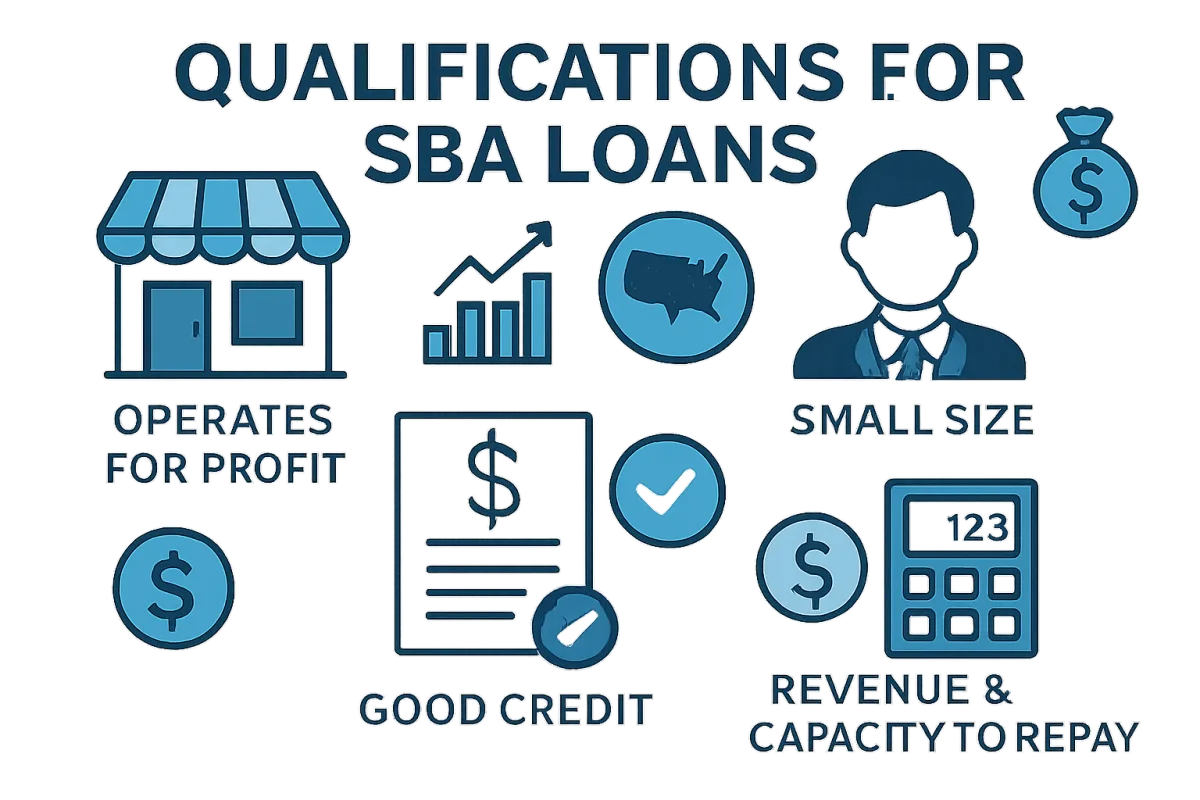

To qualify for an SBA loan, applicants typically need to meet several criteria, including being a for-profit business, having a sound business purpose, and demonstrating the ability to repay the loan. Additional requirements may include a minimum credit score, a certain amount of business equity, and a detailed business plan. The specific qualifications can vary based on the type of SBA loan being applied for.

Quick Summary

SBA loans are designed to support small businesses, but qualifying for them requires meeting specific criteria. Key factors include business type, creditworthiness, and financial history. Understanding these requirements can help streamline the application process.

Curator Notes

SBA loans are a popular financing option for small businesses, but qualifying can be a complex process. Generally, applicants must be for-profit businesses operating in the U.S. and must demonstrate a legitimate need for the funds, such as purchasing equipment or expanding operations.

Additionally, the SBA looks for businesses that have a feasible business plan and can show the ability to repay the loan from future cash flow. Creditworthiness is another critical factor. Most lenders require a minimum credit score, often around 650, although some programs may allow for lower scores under certain conditions.

Furthermore, applicants must provide personal and business financial statements, including tax returns, to demonstrate their financial health. Understanding these requirements can significantly enhance your chances of securing an SBA loan.

Recommended Options

- 7(a) Loan Program: Best for General small business needs Offers flexible financing options for various business purposes. Signal checked: Widely used by small businesses across the U.S. Alternative to consider: 504 Loan Program for real estate purchases.

- 504 Loan Program: Best for Real estate and equipment financing Signal checked: Preferred by businesses looking to invest in property. Alternative to consider: Microloan Program for smaller funding needs.

- Microloan Program: Best for Startups and small businesses needing less capital Signal checked: Ideal for new businesses and entrepreneurs. Alternative to consider: Personal loans for quick funding.

Best Sources

Videos and Community Signals

The SBA 7(a) Loan Program has a 420-page rulebook full of requirements, exceptions, and nuances—but in this video, we break ...

SBA Promo extended through 2026. ✨ Getting an SBA loan can be tricky, but we'll walk you through the SBA loan process.

Comparison

| Decision Point | Good Starting Choice | When to Go Further |

|---|---|---|

| Loan Amount | Microloan Program (up to $50,000) | 7(a) Loan Program (up to $5 million) |

| Purpose of Loan | Microloan for startup costs | 504 Loan for purchasing real estate |

| Credit Score Requirement | Microloan (flexible) | 7(a) Loan (minimum 650) |

FAQ

Most SBA loans require a minimum credit score of around 650, but some programs may allow for lower scores.

SBA loans can be used for various purposes, including purchasing equipment, real estate, or working capital.

Approval times can vary, but it typically takes 30 to 90 days for an SBA loan application to be processed.