HSA vs FSA Key Differences

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are both tax-advantaged accounts designed to help individuals save for medical expenses. HSAs are available to those with high-deductible health plans and allow funds to roll over year to year, while FSAs are employer-established and typically require funds to be used within the plan year. Understanding these differences can help individuals make informed decisions about their healthcare savings options.

Quick Summary

HSAs and FSAs serve similar purposes but have key differences. HSAs are linked to high-deductible health plans and allow for fund rollover, while FSAs are employer-managed and often have a use-it-or-lose-it policy. This guide explores their distinctions to aid in financial planning.

Curator Notes

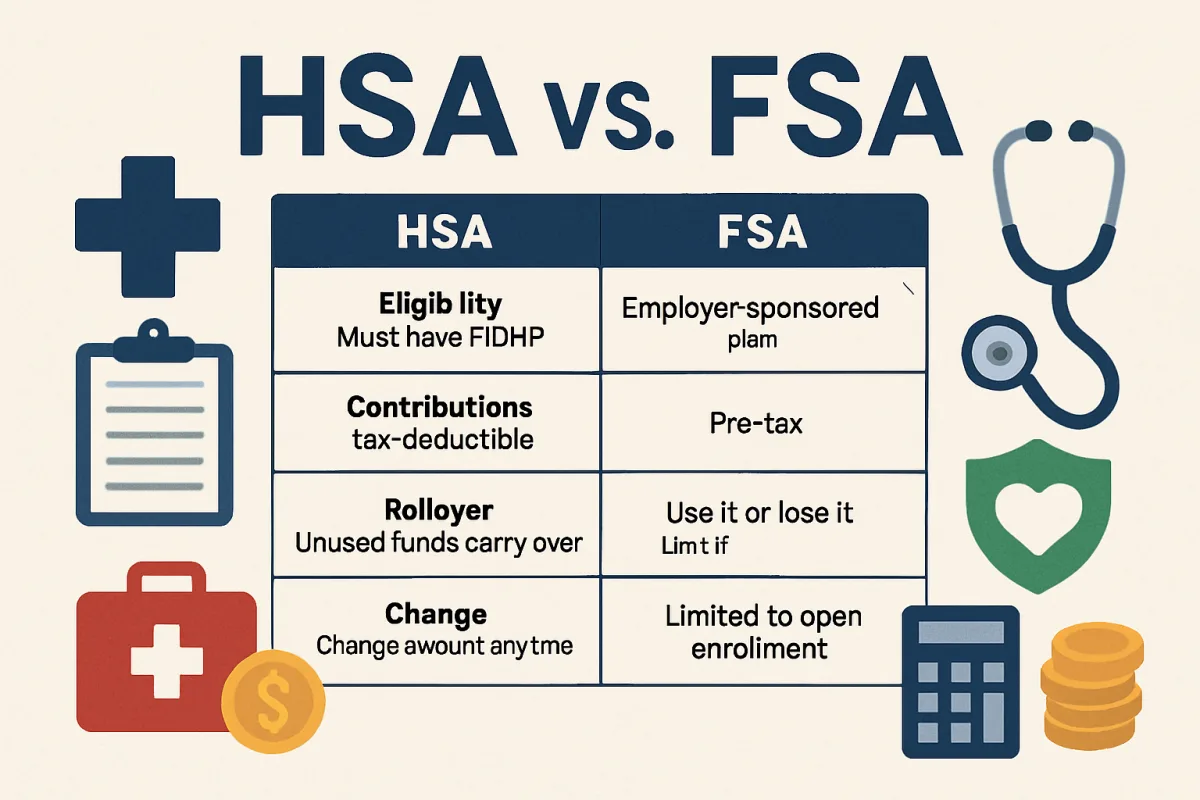

Health Savings Accounts (HSAs) are designed for individuals enrolled in high-deductible health plans (HDHPs). They allow account holders to contribute pre-tax dollars, which can be used for qualified medical expenses. One of the major advantages of HSAs is that the funds can roll over from year to year, meaning you can accumulate savings over time.

Additionally, HSAs can be invested, potentially growing your savings further. Contributions to HSAs are tax-deductible, and withdrawals for qualified medical expenses are tax-free, making them a powerful tool for long-term health savings. On the other hand, Flexible Spending Accounts (FSAs) are typically offered by employers and allow employees to set aside pre-tax dollars for medical expenses.

Unlike HSAs, FSAs usually have a use-it-or-lose-it policy, meaning any unspent funds at the end of the plan year are forfeited. FSAs can be used for a wider range of expenses, including some that HSAs may not cover, but they lack the rollover feature. Employees should carefully estimate their medical expenses to maximize the benefits of an FSA, as overestimating can lead to lost funds.

In summary, HSAs are more flexible and beneficial for long-term savings, while FSAs can be useful for predictable, short-term medical expenses. Understanding these differences can help individuals choose the right account based on their healthcare needs and financial goals.

Best Sources

Videos and Community Signals

Confused about HSA vs FSA? Wondering which one can save you more money on taxes and healthcare? In this video, I break ...

Do you know the difference between an HSA and an FSA? Clark breaks it down, helping you make the most of your healthcare ...

Comparison

| Decision Point | Good Starting Choice | When to Go Further |

|---|---|---|

| Eligibility | Available to anyone with a high-deductible health plan (HDPH) | Only available through employer-sponsored plans |

| Contribution Limits | Annual contribution limit set by IRS (e.g., $3,650 for individuals in 2023) | Annual contribution limit set by employer, usually lower than HSA limits |

| Rollover Policy | Funds roll over year to year | Use-it-or-lose-it policy; unspent funds expire at year-end |

| Investment Options | Funds can be invested for potential growth | No investment options; funds must be used for eligible expenses |

FAQ

Yes, you can have both accounts, but there are specific rules about how they can be used together, especially regarding eligible expenses.

Your HSA is yours to keep, even if you change jobs. You can continue to use the funds for qualified medical expenses.

Yes, contributions to both HSAs and FSAs are made with pre-tax dollars, reducing your taxable income.